One question we are often asked is: “When should I start planning for retirement?” The simple answer is as soon as you can. According to a famous Chinese proverb, “The best time to plant a tree was 20 years ago. The second best time is now.” The same philosophy applies to retirement planning. Ideally, you can start saving in your 20s when you graduate from school and start working. However, there are steps you can take at any stage of life to help you on your way to retirement.

Planning for retirement is an ongoing process that requires thoughtful consideration and action throughout the different stages of one’s life. Establishing savings goals by age can help individuals to secure a comfortable and financially stable retirement. Below are some age-specific retirement savings benchmarks that can guide you in making well-informed decisions.

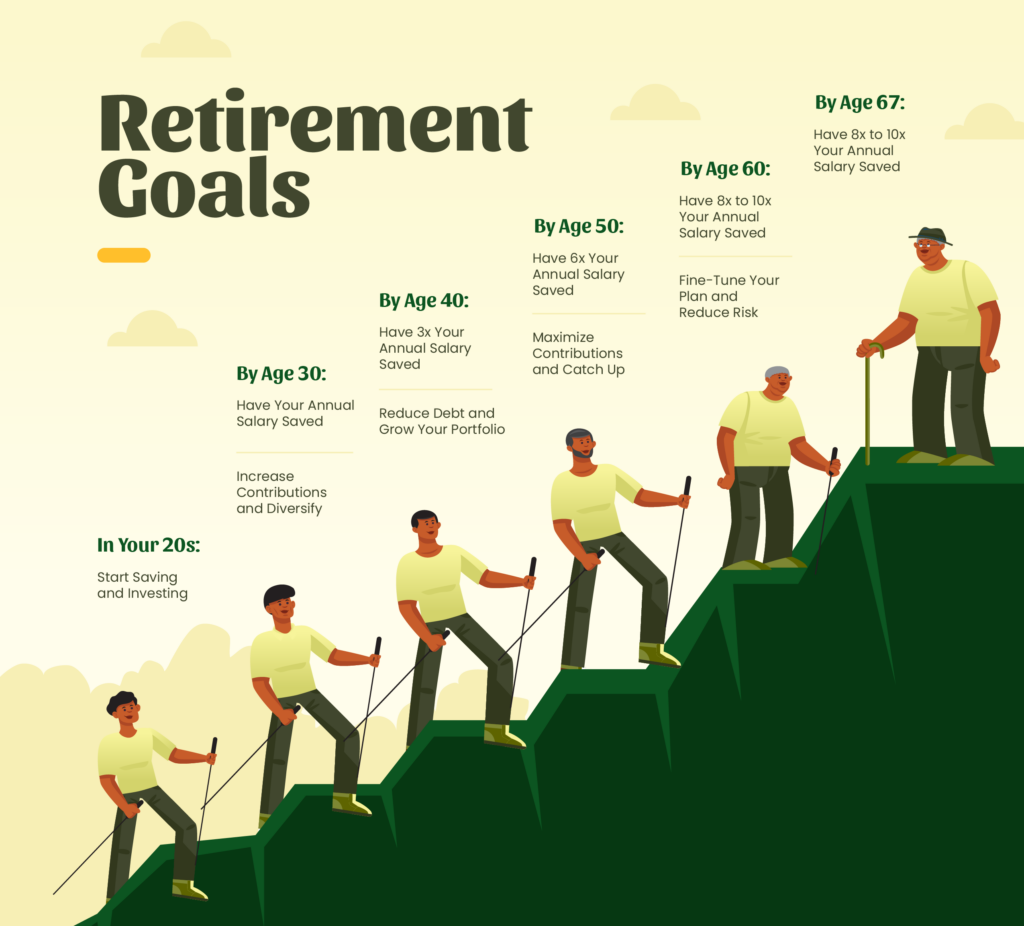

In Your 20s: Start Saving and Invest in Retirement Accounts

When you’re in your 20s, retirement seems a long way off. However, this is the perfect time to start saving due to the power of compounding. Aim to save at least 10% to 15% of your income. If your employer offers a 401k match, contribute enough to take full advantage of this. Also, consider opening an IRA (Individual Retirement Account) to diversify your retirement savings.

By Age 30: Have the Equivalent of Your Annual Salary Saved

By the time you hit 30, a good benchmark is to have the equivalent of your annual salary saved for retirement. For instance, if you earn $50,000 a year, aim to have $50,000 in retirement savings.

In Your 30s: Increase Contributions and Diversify Investments

In your 30s, your income is likely to increase, and your financial situation might become more stable. Strive to increase your retirement contributions gradually. Additionally, diversify your investment portfolio by considering different asset classes like stocks, bonds, and real estate. By age 40, aim to have three times your annual salary saved.

In Your 40s: Focus on Debt Reduction and Portfolio Growth

In your 40s, it’s essential to focus on reducing high-interest debt such as credit card debts. This is also the time to review and perhaps rebalance your investment portfolio to ensure it aligns with your risk tolerance and retirement goals. By the age of 50, strive to have six times your annual salary in retirement savings.

In Your 50s: Maximize Contributions and Consider Catch-up Contributions

This is a critical decade for retirement savings. The IRS allows individuals aged 50 and over to make catch-up contributions to retirement accounts. Maximize your contributions to 401(k)s and IRAs. Start thinking about the lifestyle you want in retirement and estimate the costs associated. By age 60, aim to have eight to ten times your annual salary saved.

In Your 60s: Fine-Tune Your Retirement Plan and Reduce Risk

As you approach retirement, it’s time to fine-tune your retirement plan. Consider meeting with a fee-only financial planner to discuss withdrawal strategies and tax planning. Gradually reduce the risk in your investment portfolio by shifting to more conservative investments. It’s also a good time to investigate Social Security benefits and decide on the optimal time to start taking them.

By Age 67: Aim to Have 10 to 12 Times Your Annual Salary Saved

By the time you reach full retirement age, which is 67 for many people, aim to have 10 to 12 times your final salary in retirement savings. This amount, combined with Social Security benefits, should provide a comfortable standard of living throughout your retirement years.

In Retirement: Manage Withdrawals and Monitor Investments

Once retired, carefully manage your withdrawals to ensure that your savings last throughout your retirement. A common rule of thumb is the 4% rule, which suggests withdrawing 4% of your retirement savings in the first year and adjusting that amount for inflation in the following years. It’s also crucial to continue monitoring your investments and consulting with a financial advisor to make sure your financial strategy adapts to your needs as they evolve.

In conclusion, it’s important to recognize that these benchmarks are general guidelines. Individual circumstances vary, and life can sometimes throw unexpected challenges your way. What’s most important is to consistently save and invest wisely, regardless of where you are in life, and to be adaptable in your planning. Regularly assess your retirement goals and make necessary adjustments to ensure you are on track to achieve the retirement lifestyle you envision.

When Do People Normally Retire?

Reading statistics about the average retirement age doesn’t necessarily provide any meaningful insight into determining the best time for your own retirement.

It is true that a majority of individuals we work with tend to retire between the ages of 62 and 70, but it is crucial to recognize that each case is unique. In figuring out your own retirement timeline, your decision should be informed by reflecting on these questions:

- At what point will I be able to comfortably stop working?

- Should I consider a phased retirement or complete retirement?

- Is my physical well-being good enough to continue to work?

- Do I still get fulfillment and stimulation from my work?

- What is my vision for retirement? How do I intend to occupy my time?

- Would I favor prolonging my working years and securing a more affluent retirement, or retire earlier and adopt a more modest lifestyle?

Once you have considered these questions, you can then start to formulate a timeline for your retirement.

Contact a Retirement Planner Today

As fee-only certified financial planners and fiduciaries, we help our clients with all aspects of retirement, from financial planning to living a full, happy life through our Enrichment Program. Our Comprehensive Guide to Retirement Planning has helpful information on more topics. If you have questions about retirement savings goals by age or how to plan for the retirement you’ve always envisioned, contact Zynergy Retirement Planning today for a free consultation.